The price of crude oil tanked today as Russia rejected steeper supply cuts that OPEC had suggested. In a ministerial meeting yesterday, OPEC leaders agreed to cut 1.5 million barrels a day until the end of the year. A senior Russian official told Reuters that the country would not accept such a proposal. Instead, the country will only accept an extension of existing cuts. There are two main reasons why Russia is opposed to these cuts. First, the country wants to limit the existing market share by the United States. Second, Putin wants to maximize his geopolitical leverage to punish Middle East countries that are part of OPEC. As a result, these countries will likely ask him to agree to cuts and then ask for concessions elsewhere.

Global stocks continued falling while bonds rose on fears of a global economic meltdown caused by a coronavirus. In the US, futures tied to the Dow and Nasdaq declined by more than 2%. In Europe, the Stoxx, DAX, and CAC declined by more than 3%. In Asia-Pacific, the ASX, A50, and Nikkei dropped by 2.80%, 1.77%, and 2.72% respectively. Investors are worried about the catastrophic spread of the disease. Already, the number of those infected has crossed the 100k mark while the number of those who have died has reached 3,000. In China, the rate of the disease spread has reduced but many companies have struggled to reopen. Also, thousands of flights remain grounded.

The US dollar declined today even after robust employment data from the government. The data showed that the economy added more than 273k jobs in February. This was higher than the expected increase of 175k. The private nonfarm payrolls increased by 228k while the unemployment rate dropped to a 50-year low of 3.5%. The average number of hours worked increased from 34.3 to 34.4 while wage growth declined from 3.1% to 3.0%. On trade, the country exported goods worth more than $208.6 billion down from $209 billion. It imported goods worth $253 billion leading to a deficit of $45.3 billion. While these numbers are good, traders are focused on the action by the Fed, which is expected to slash interest rates later this month.

XBR/USD

The XBR/USD pair declined to 46.81, which is the lowest it has been since July 2017. This price is lower than the short, medium, and long-term moving averages while the accumulation/distribution indicator continued to decline. The same is true with the on-balance volume. The pair will likely continue to decline as demand falls while supply continues to rise.

XAU/USD

The XAU/USD pair rose to an intraday high of 1690.10. The pair has had the best week since May 2016 as investors move to safe-havens. The rise has also been because of the rate cut by the Federal Reserve on Tuesday and the one anticipated later this month. The price is along the upper line of the Bollinger Bands while the RSI is above the overbought level of 70. The pair will likely continue to rise ahead of the next Fed meeting.

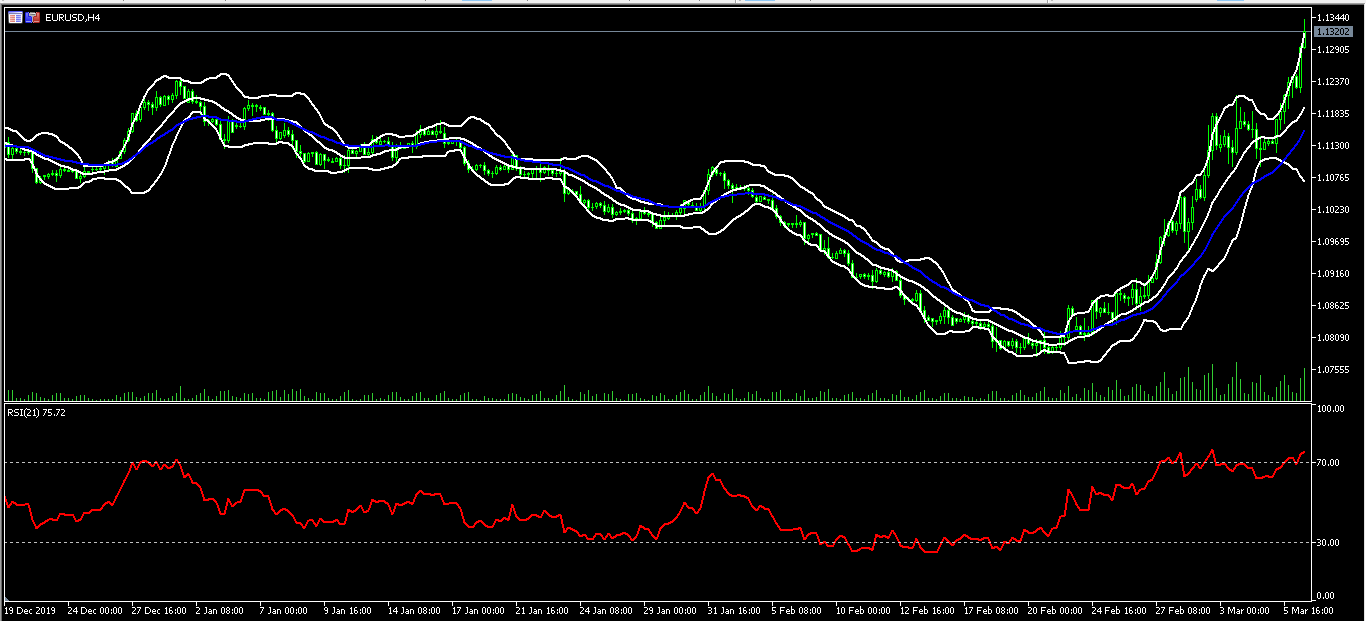

EUR/USD

The EUR/USD pair rose to an intraday high of 1.1338, which is the highest level since July last year. The pair has been on an upward trend since February 20 when it was trading at 1.0775. The price is along the upper line of the Bollinger Bands and above the short and long-term moving averages on the four-hour chart. The RSI has remained above the overbought level of 70. While the pair may continue rising, there is also a possibility of this changing in the coming week.