- DXY adds to Tuesday’s gains and moves to weekly highs.

- Higher yields undermine the recent upbeat sentiment in the risk complex.

- Retail Sales, Industrial Production next of note in the US docket.

The greenback, in terms of the US Dollar Index (DXY), advances further and already trades at short distance from the key barrier at 91.00 the figure.

US DOLLAR INDEX LOOKS TO DATA, YIELDS

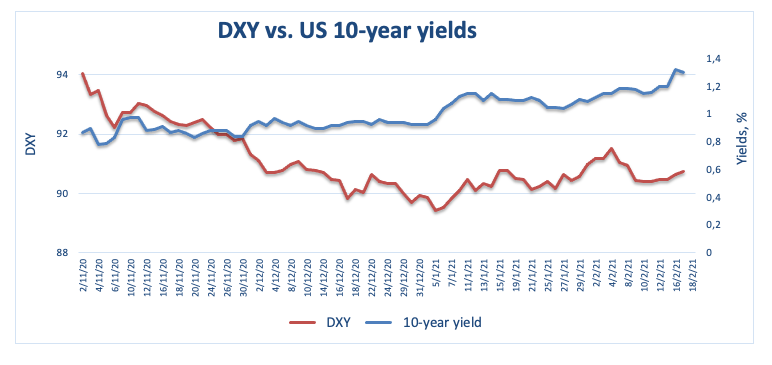

The index trades on a better tone and advances for the second session in a row on Tuesday, leaving behind minor resistance levels at the 21-day SMA (90.63) and the 10-day SMA (90.75).

The march higher in US yields has been sustaining the rebound in the dollar as of late. In fact, yields of the key 10-year reference surpassed the 1.33% level on Tuesday, area last seen in February 2020, as investors continue to gauge the pick-up in the inflation vs. extra fiscal stimulus and higher energy prices.

In the domestic docket, the focus of attention will be on January’s Retail Sales seconded by Industrial Production figures and the FOMC minutes. Other secondary releases include the weekly MBA Mortgage Applications, monthly Business Inventories, Capacity Utilization, the API’s report and the NAHB Index.

Additionally, Richmond Fed T.Barkin (voter, centrist) and Boston Fed E.Rosengren (2022 voter, hawkish) are due to speak.

What to look for around USD

The corrective downside in the index appears to have met a decent support near the 90.30/20 band recently. The price action in the dollar recovered the positive correlation to US yields, allowing the ongoing rebound to the vicinity of the 91.00 yardstick. However, bullish attempts in the buck should remain short-lived, amidst the broad fragile outlook for the currency in the medium/longer-term. In the meantime, the current massive monetary/fiscal stimulus in the US economy, the “lower for longer” stance from the Fed and prospects of a strong recovery in the global economy are forecast to keep underpinning the better sentiment in the risk-associated space.

Key events in the US this week: January’s Retail Sales, Industrial Production and the FOMC Minutes (Wednesday). Weekly Initial Claims and the Philly Fed Index are due on Thursday ahead of flash PMIs (Friday).

Eminent issues on the back boiler: US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating? Future of the Republican party post-Trump acquittal.

US Dollar Index relevant levels

At the moment, the index is gaining 0.26% at 90.74 and a breakout of 91.55 (100-day SMA) would open the door to 91.60 (2021 high Feb.5) and finally 92.46 (23.6% Fibo of the 2020-2021 drop). On the other hand, initial support lines up at 90.22 (weekly low Feb.16) followed by 90.04 (weekly low Jan.21) and then 89.20 (2021 low Jan.6).